Good organic revenue growth

in first half of year

Quarterly Overview

Good organic revenue growth in first half of year

Solid uptrend of Telecom confirmed, High Voltage Underground and Trade & Installers also grew. Integration with General Cable started in record time and first synergies from procurement and reorganisation yielded.

The Board of Directors of Prysmian Group has approved the consolidated results for the first half of the year with positive business performances leading to a good organic revenue growth. CEO Valerio Battista remarked that profitability was affected by the impact of provisions for the Western Link project, but net of such provisions, the profitability of the Projects business was stable. The most significant contribution to Adjusted EBITDA was attributable to the margins improvement of the Telecom business.

The CEO also stated that the integration with General Cable started in record time, with the launch of the new organisation just 10 days after the closing on 6 June 2018, along with the rapid commencement of work for the procurement area and of organisational streamlining. Expected synergy targets were thus confirmed at €150 million, with impacts as early as 2018 year-end results. For the remainder of the year, the Group confirmed the forecasts for full-combined adjusted EBITDA in the range of €860 and €920 million.

Claudio De Conto was appointed Chairman of the Board of Directors after the previously announced resignation of Massimo Tononi, while Francesco Gori became a new member of the Board of Directors.

Sales

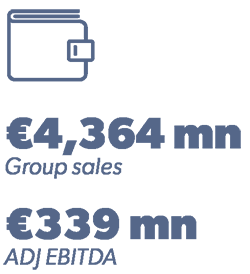

Group sales amounted to €4,364 million, of which €381 million are attributable to General Cable, with a 2% organic growth vs H1 2017. The Telecom business confirmed a solid uptrend while High Voltage Underground and Trade & Installers also posted growth.

Adjusted EBITDA

Adjusted EBITDA came in at €339 million, of which €25 million is attributable to General Cable, which was consolidated for June 2018 only. The decrease compared to H1 2017 was essentially attributable to the €70 million provisions for issues concerning the execution of the Western Link project, and to the effects of exchange rates.

Net Financial Debt

Net financial debt amounted to €3,014 million as of 30 June 2018, from €436 million as of 31 December 2017, benefitting from the conversion of the 2013 convertible bond with an impact of €283 million. The main factor influencing the figure was the acquisition of General Cable, amounting to €2,547 million, made up of the share price paid, debt refinancing and transaction costs.

Guidance

The Group forecasts an adjusted EBITDA within a range of €860-920 million for 2018, up from the €733 million reported in 2017. This includes the results of the General Cable business for all of 2018, in addition to the provision of €70 million for the Western Link project (recognised in the first half of the year).

Energy Projects

Organic growth up 1.8%

Positive performances of the High Voltage Underground business in APAC, Southern Europe and South America markets. Planning progress and greater visibility on the timing of the HVDC ‘corridors’ SüdLink and SüdOstLink in Germany.

Energy Projects sales (excluding General Cable perimeter) reached €684 million in H1 2018, with an organic growth of +1.8%. Adjusted EBITDA was €50 million, negatively impacted by provisions for the Western Link project, excluding which, it was €120 million. Adjusted EBITDA ratio-to-sales was 7.4% from 17.2% for H1 2017.

In the Submarine business, the Group continued its major projects already underway, including both offshore wind farm interconnectors, and particularly improving its installation capacities thanks to investments made in new assets and technologies. The market recorded a tendering slowdown with the postponement of some large projects scheduled towards the end of 2018 and 2019. The commissioning and testing of the Western Link Interconnector had been temporarily interrupted due to the need to investigate a problem occurring in the onshore section.

In the High Voltage Underground business, the positive results were driven chiefly by the sharp growth in demand in Asia Pacific, Southern Europe and South America, which offset weakness in the UK and the Netherlands during the same period. Significant progress in the execution of HVDC projects in Europe is also noteworthy.

The power transmission order book totalled €2,150 million. In the Submarine business, tendering activities are expected to accelerate in H2 2018 and in 2019, whereas in the High Voltage Underground business the procurement process has started for major SüdLink and SüdOstLink interconnection projects in Germany, with greater visibility of the timing of their launch.

Energy Products

T&I improved, with an uptrend for Industrial & NWC

T&I organic growth trend improved, with volumes recovery in Q2 in Europe and North America, while Power Distribution volumes were stable. Organic uptrend confirmed for Industrial & NWC.

Energy Products sales, excluding GC perimeter, increased 1.6% to €2,521 million, mainly due to volumes growth in Europe, while adjusted EBITDA came in at €120 million, down from €135 million in H1 2017. This was mainly due to the negative effect of exchange rates and the unfavourable business trend in the Middle East. Energy & Infrastructure sales amounted to €1,681 million, +0.2% organically, with adjusted EBITDA at €61 million, and a ratio-to-sales of 3.6% compared to 4.5%.

Trade & Installers showed an uptrend, improving in Q2, driven by a recovery of volumes in North America and a continued positive performance in Europe, particularly in Germany, the Netherlands, Italy and Spain. A profitability decrease was partly offset by the entrance into effect of the new Construction Products Regulation in all EU countries, and a general volumes recovery in Europe. Power Distribution reported positive performances in France, Italy, Northern Europe and Oceania, with a stabilisation in Q2 after the slowdown earlier in the year. Unfavourable exchange rates and weakness in the Middle East affected profitability.

Industrial and Network Components sales grew 4.8% organically to €764 million, with adjusted EBITDA at €59 million compared to €62 million in H1 2017, and a ratio-to-sales at 7.7% from 8.3%. Specialties, OEMs & Renewables reported positive sales performance, stabilising in Q2, with a sharp growth of Railway and Rolling Stock and the recovery of Crane, whereas Nuclear and Mining revealed a slowdown. The Elevators business reported an acceleration of organic growth in Q2, driven by the growth in the EMEA area and volumes recovery in North America and South America, despite the weakness of the APAC market. Network Components posted a solid performance thanks to increased volumes in China and the Medium Voltage success in North America.

Oil & Gas

Growth improved sharply in Q2

Excluding GC perimeter, organic growth jumped 9.9% in the second quarter, while onshore activities improved in North America and the Middle East. Profitability also improved, DHT volumes grew thanks to solid demand.

For the entire H1 of 2018, sales amounted to €134 million, with 0.8% organic growth, while adjusted EBITDA was €3 million, slightly improving compared to €2 million in H1 2017, with a ratio-to-sales of up to 1.9% from 1.1%. The Core Cables Oil & Gas business showed an improvement in onshore projects, particularly Petrochemical, Refinery and LNG, in North America and the Middle East. The adjusted EBITDA improvement was attributable to a reduction in fixed costs and design-to-cost initiatives.

The performance of the Subsea Umbilicals, Risers & Flowlines (SURF) business improved in Q2, after a negative year-start, thanks to the favourable phasing of the projects underway in Brazil. Demand grew in Downhole Technology, mainly thanks to the step-up of shale oil and shale gas production in North America and the Middle East, where the offshore market showed small signs of improvement.

Telecom

Profitability up substantially

Adjusted EBITDA jumped 29.7%, driven by strong demand for optical cables and industrial efficiency improvement, while the uptrend in Optical & Connectivity sales continued, thanks to demand in the USA and France. Solid MMS performance.

Telecom sales, excluding GC perimeter, grew 4.4% organically to €645 million, mainly driven by the constant growth of demand for optical and multimedia solutions, with adjusted EBITDA up 29.7% to €141 million and margins improved also, with a ratio-to-sales reaching 21.8% compared to 16.8% for H1 2017. The increased profitability benefitted from fibre manufacturing process efficiencies and the optimisation of production footprint, particularly in the growth of volumes produced in the Slatina plant, Romania, in addition to the positive results achieved by the subsidiary YOFC in China and the release of the bad-debt provision for a receivable due from a Brazilian customer.

In the Telecom Solutions business, the Group was awarded important projects by the main operators in Europe for the construction of backhauls and FTTH links. In North America, the development of new ultra-broadband networks is generating a constant rise in demand, testified by the three-year agreement worth $300 million signed with Verizon. In order to further strengthen its competitive position, the Group has launched a three-year investment plan for a total of €250 million to step up production capacity and efficiency. The high value-added business of Optical Connectivity Accessories continued to perform well, particularly in France, while Multimedia Solutions volumes rose and margins improved, particularly in Europe, with demand driven by growing investments in data centres.

THE MARKET REACTION

The market was positively surprised by the strength of H1 2018 results, being well ahead of analysts’ expectations and mainly driven by higher than expected results of the newly-acquired perimeter of General Cable and a solid upward trend in the Telecom business. On top of this, the confirmation of FY2018 Outlook was particularly appreciated by the market, especially after the recent difficulties of the Western Link project.

All analysts confirmed their view on the stock following H1 2018, with a few adjusting their target price valuation of Prysmian shares. The Bank of America confirmed its view on the stock with a rating ‘BUY’, keeping the target price of 30 Euro/share unchanged. JP Morgan and Kepler reiterated this positive evaluation, confirming the target price of 28 Euro/share.

Equita and Intermonte SIM SpA have stuck to their prudent view, rating the stock as ‘HOLD’; despite the solidity of H1 2018 results and the attractive valuation, both brokers see some uncertainties surrounding the Energy Projects business.

High Voltage expected to recovery

The Group also expects an increase in demand in the Cyclical Construction and Industrial Cables businesses, while aiming to retain its leadership in Submarine. Growth has remained solid in the Telecom business.

Global economic growth remained positive in the first half of 2018, with a sharp acceleration in the United States in the second quarter, and China continuing the positive trend seen at the beginning of the year. Growth in Europe, while positive, remains slower. In Brazil too there were signs of slowing, due to inflation and pressure on exchange rates.

Prysmian Group expects an increase in demand in the Cyclical Construction and Industrial Cable businesses, driven by the recovery of European demand, while the Medium Voltage Utilities Cable business is expected to remain essentially stable. In Submarine Cables and Systems, despite the slowdown in the award of contracts in the first half, the Group aims to retain its leadership and its share in a recovering market, with an increase in the volume of projects awarded in the second half of the year.

The Group expects High Voltage Underground Cables and Systems to recover with a gradual improvement in performance in China and South East Asia. It also foresees that growth will remain solid in Telecom, supported by growing demand for optical cables in Europe and North America.

In light of these considerations, the Group forecasts an adjusted EBITDA within a range of €860-920 million for all of 2018, an increase on the €733 million reported in 2017. The forecast includes the results of recently acquired General Cable. Excluding the effects of the acquisition of General Cable, the Group expects to record an adjusted EBITDA for all of 2018 of between €680 million and €720 million, compared to the €733 million recorded in 2017.